Listen to this article

"How to Get a Mortgage With Less Than 2 Years of Self-Employment"

How to Get a Mortgage With Less Than 2 Years of Self-Employment

If you are self-employed and trying to buy a home, you have probably heard this line:

“You need two years of self-employment history.”

That is often true, but it is not always as strict as it sounds. The real question lenders are trying to answer is simple:

Let's Talk About Your Goals

Have questions about this topic? Robert Garrod is here to help you understand your options and guide you through the process.

Can we reasonably expect your income to continue?

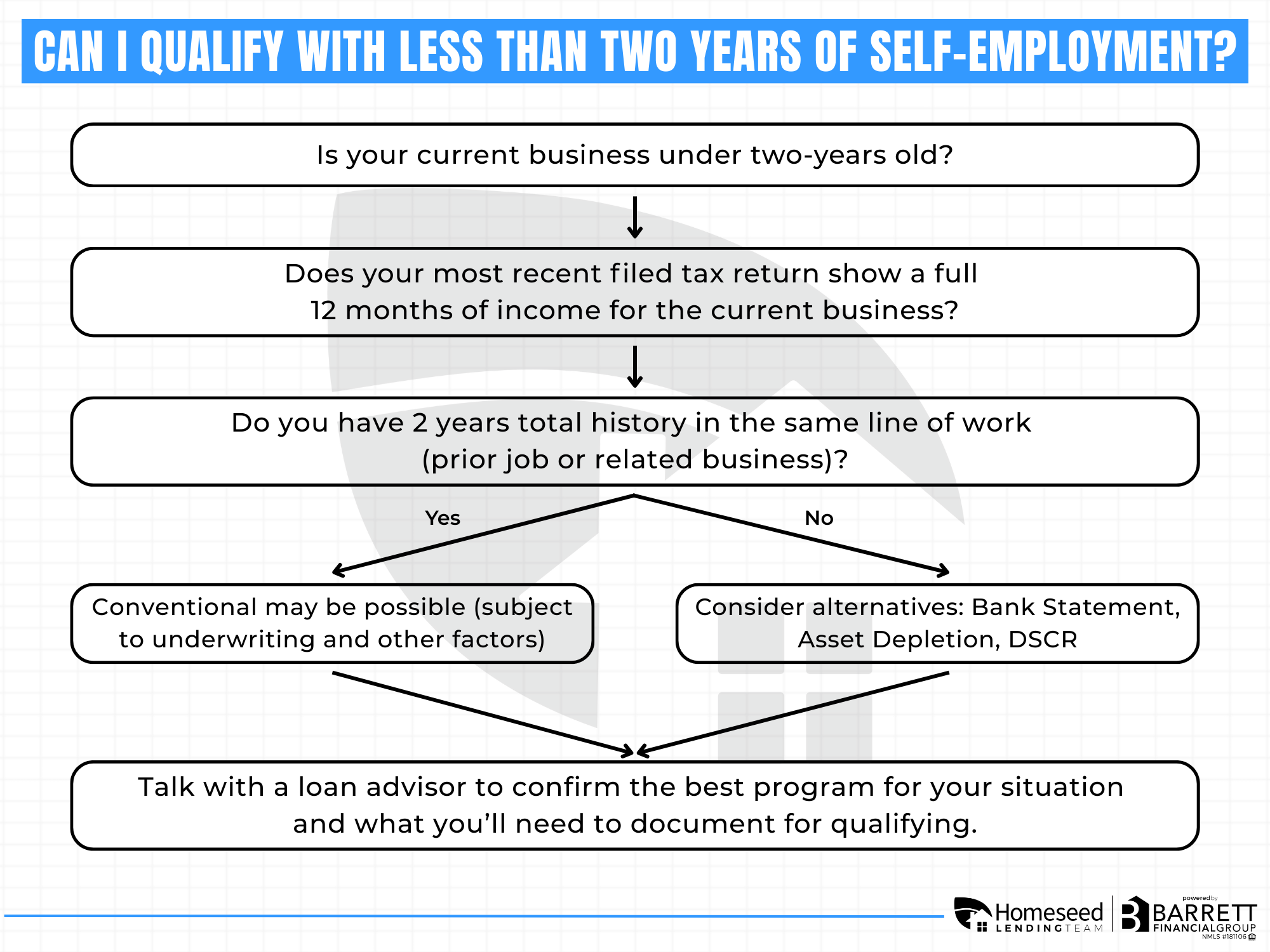

If your business has been open for less than two years, you may still be able to qualify, especially if you can show a full year of income in the business and a strong work history leading up to it.

Conventional Financing Guidelines for Self-Employed Borrowers

Most conventional mortgage guidelines follow a similar logic:

1) You typically need at least one full year of documented business income

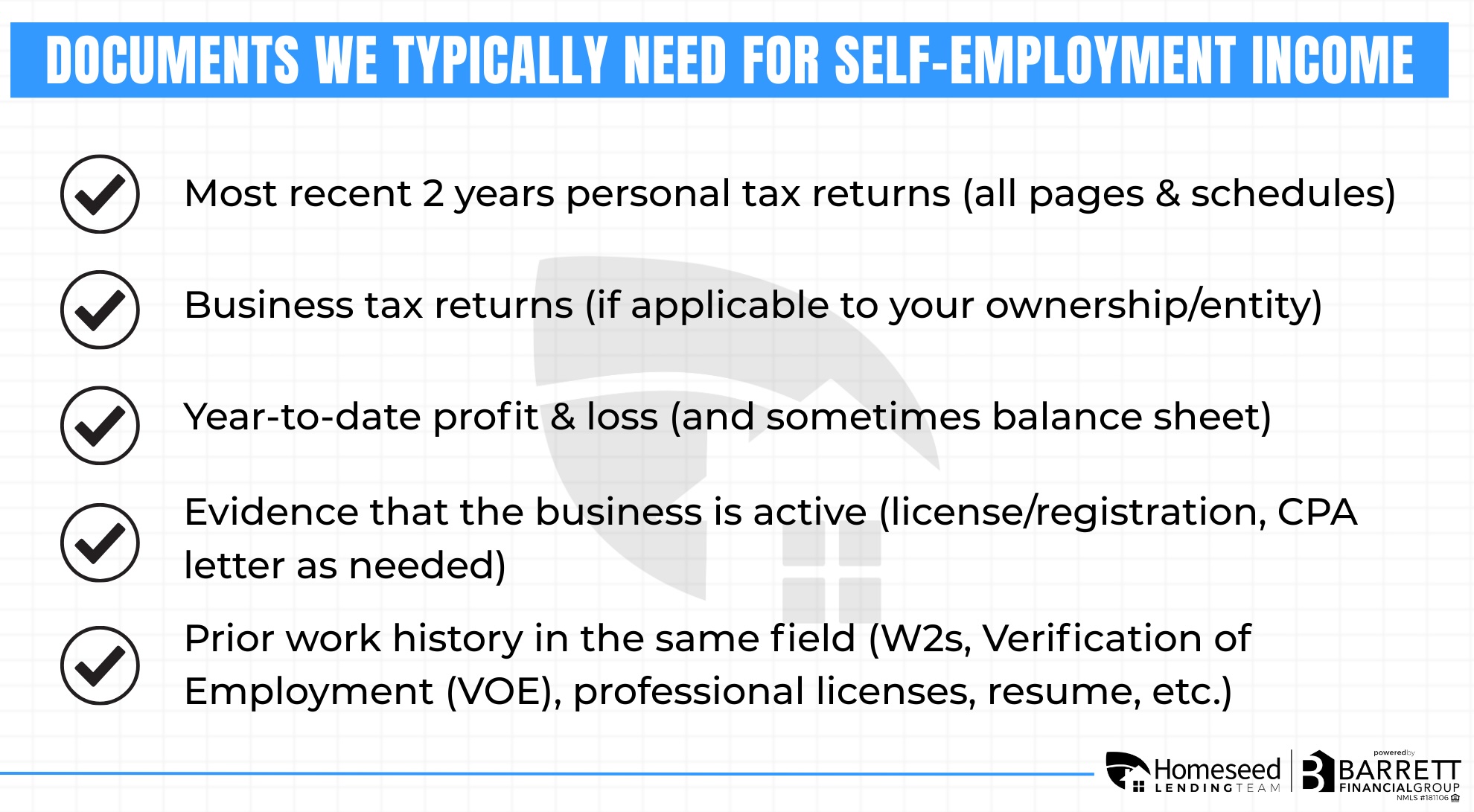

Even if you have filed two tax returns, lenders usually want to see that your most recent tax return shows a full 12 months of self-employment income from your current business.

This is a big deal because a partial first year (for example, 6 months of income on the first return) does not automatically prove consistency yet.

2) You still need a 2-year track record overall

If your business has not been around for two full years, lenders will usually look at your background to fill in the gap. That “missing” history can often come from:

- A prior job in the same field (W-2 income), or

- Similar work with similar responsibilities, or

- Another prior business that is closely related

In simple terms, if you have been doing the same type of work for a while and recently switched into running your own business doing that same work, lenders may be able to treat your income as more stable than someone who started a brand-new career and a brand-new business at the same time.

What Happens if I Have Less Than Two Years

A common example we see is, “I have two years of tax returns, but the business is only 18 months old because year one only shows 6 months. Do I have to wait until I hit two years in business?”

Not necessarily.

If your most recent tax return covers a full 12 months of income from the business, and you can show you have been in the same line of work before the business started, there is often a path forward.

Supporting Factors to Help You Get Approved

Even for a general rules approach, these are the big items that can help you qualify:

- You have at least one full year of business income documented on tax returns

- Your work history before the business supports that this is the same type of work

- Your income trend looks stable (or you can explain a dip clearly)

- Your credit, savings, and overall debt look solid

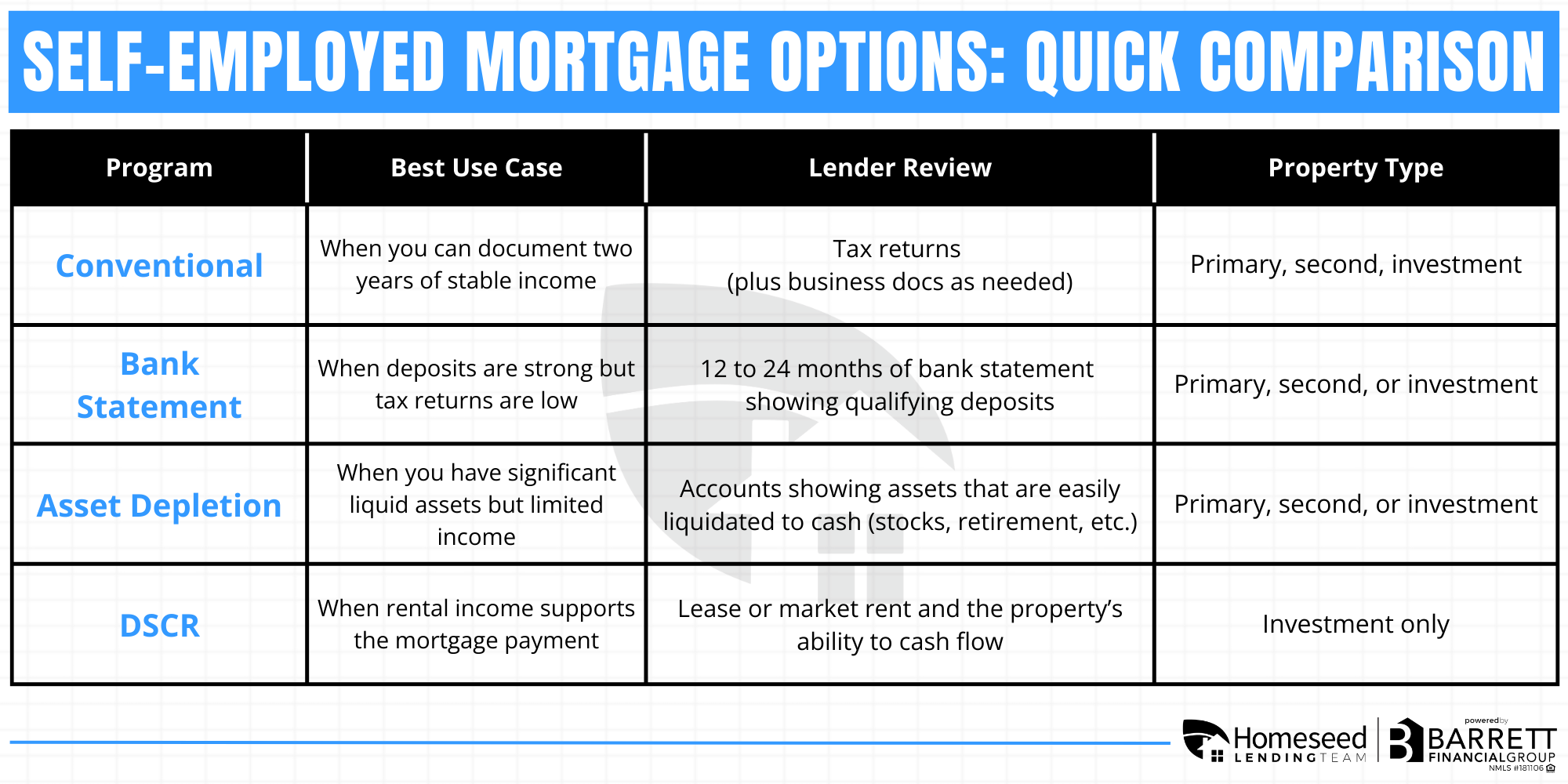

Are There Other Programs Available?

If the tax returns do not show a full 12 months for the current business, or the income is too new to use, there are still options depending on your scenario:

- Bank statement loan options (often used by self-employed borrowers who write off a lot)

- Asset-based qualification (for high-asset borrowers)

- DSCR loans for investment properties (qualifies based on rental cash flow, not personal income)

Ready to See What You Qualify For?

If you are self-employed and your business is under two years old, the best first step is a quick strategy call. In a short conversation, we can help you understand:

- Whether you can qualify now with a conventional loan using your history and most recent tax return

- If not, which alternative program (like bank statements) might fit better

- What steps to take over the next few months to improve approval odds

This blog post is intended for informational purposes only. It does not constitute financial advice, an offer to extend credit, or a commitment to lend. Mortgage rates, program guidelines, and qualification requirements can change at any time and may vary based on credit, income, assets, location, and property type. Always consult with a licensed mortgage broker to review your personal situation and available options.

Topics

Enjoyed this article?

Share it with your network